In recent years, private capital investors have increasingly focused on businesses underpinned by strong client relationships, resilient demand and recurring mandates. This has resulted in a growing willingness to back professional services businesses, with the accountancy sector leading the way through a number of high-profile transactions.

Recent activity in the UK market indicates that the legal services industry is now beginning to attract similar attention. However, the legal sector remains fundamentally different from many of the businesses with which lenders and investors are typically more familiar and, whilst third-party investment is becoming increasingly accessible to law firms, the sector’s structural realities mean that securing outside capital remains far from straightforward.

In this Deep Dive article, Daniel Hendon (Partner) and Charlotte Boylin (Special Finance Counsel) in Proskauer's Private Credit Group in London explore the evolution of private capital investment in legal services, examine some of the key differences between two innovative structures that enable external investment into the legal sector – notably, Alternative Business Structures (“ABSs”) and Management Services Organisations (“MSOs”), and outline certain legal and practical considerations for stakeholders assessing a possible investment within the sector.

The old model is no longer enough

Historically, law firms have relied on a conservative funding model – not only because of the complexities associated with investing in law firms, but also because the legal framework restricted the scope for outside ownership. Before the implementation of the Legal Services Act 2007 and the introduction of ABSs, non-lawyer ownership of law firms in England and Wales, and therefore the ability to attract external investment, was highly constrained. Growth was instead typically financed through partner capital contributions, retained earnings and cautious balance sheet management - that approach reflected both professional culture and practical necessity.

That traditional funding model is now under increasing pressure and advances to the legal framework which now enable law firms to obtain external investment have therefore been important. Modern law firms face investment demands that are materially larger and more urgent than those faced by earlier generations. Technology has become central to competitiveness, including in relation to AI-enabled workflows, cybersecurity, matter management systems, pricing tools and broader digital infrastructure. Talent has also become more expensive: lateral hiring, team acquisitions and retention strategies all require capital, whilst firms pursuing expansion, consolidation or platform-building strategies need funding for acquisitions, integration and working capital.

As these financial pressures increase, internal funding alone is often insufficient. Third-party investment has therefore begun to look less like an anomaly and more like a practical response to the changing demands of legal practice.

A changing landscape: the institutionalisation of legal services

The UK’s ABS regime has been a critical enabler for investment in the legal sector. By permitting external ownership and non-lawyer participation in legal businesses, ABSs created a framework through which private capital could participate directly in the sector. This has materially changed the investment case: legal businesses can now be owned, governed and financed in a more corporate manner, making them easier for private equity sponsors and lenders to analyse, capitalise and support.

Recent UK transactions show that private capital is entering the sector through a variety of routes. August Equity’s investment in Higgs LLP reflects confidence in the platform potential of a regional law firm, whilst Inflexion’s acquisition of DWF shows that private equity is also prepared to support larger legal and business services models with broader reach and more diversified revenue streams. The significance of these deals lies not only in the businesses involved, but in what they reveal about market confidence. Private capital is no longer merely testing the edges of legal services - it is moving into the sector more deliberately just as it has done in accountancy services.

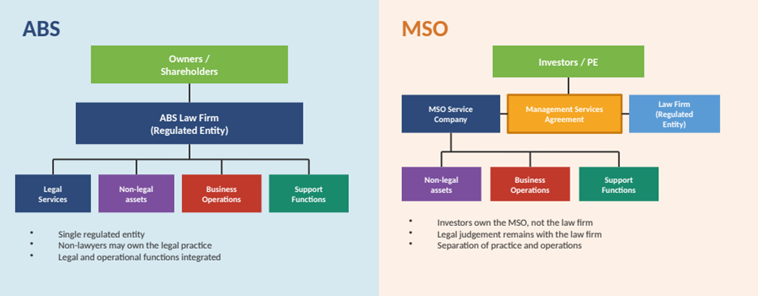

Structural considerations: ABSs and MSOs

Whilst the ABS framework can provide an effective mechanism for facilitating direct investment in English law firms, it is not always a viable solution for firms operating across multiple jurisdictions. Many jurisdictions continue to prohibit non-lawyer ownership or control of regulated legal practices under their professional regulatory regimes. In those circumstances, an MSO structure can offer a practical alternative by enabling external investment and operational integration whilst preserving compliance with local regulatory requirements.

Taking these structures in turn, an ABS is a regulated legal practice in which non-lawyers can own, invest in and/or manage the law firm itself, and is licensed by an approved regulator such as the Solicitors Regulation Authority. Because ABSs permit direct investment in regulated legal practices, investors can acquire equity ownership, deploy growth capital and participate directly in value creation. The ABS framework also supports scalable growth, strategic acquisitions, management professionalisation and integrated service offerings, making it an attractive platform for buy-and-build and consolidation strategies within the legal sector.

In contrast, an MSO is generally a separate business that provides administrative and operational support services and holds non-legal assets such as technology, IP, HR and other non-legal employees. Within the law firm context, the law firm remains lawyer-owned (where required by regulation), whilst the MSO may be owned by non-lawyers or investors and the relationship between the two is governed by a management services agreement. Private equity investors are attracted to MSO structures because they can provide centralised and recurring revenue streams, support the creation of scalable EBITDA and facilitate multi-firm consolidation strategies without requiring direct ownership of law firms operating in jurisdictions where that ownership is restricted. Investment capital is typically deployed at the MSO level rather than into the regulated legal practice, positioning the MSO as the platform entity through which affiliated firms operate within a broader integrated network.

The diagrams below display a high-level comparison of these structures:

Investing in the legal sector: other key considerations

As with any investment case, legal and practical risks need to be considered, and the legal sector presents certain features which make the investment analysis more complex than in many other business sectors. From a debt perspective, lenders typically favour strong collateral, regular cash conversion and organisational structures that align with standard underwriting models. Law firms often present a different profile: limited hard assets, irregular working capital cycles and partnership dynamics that can make capital retention more difficult. Here we delve into some other important considerations:

- Timing - Law firms often incur costs immediately but receive revenue much later. Salaries, rent, insurance and technology costs must be paid in real time, whilst fee income may be delayed by billing practices, client approval processes, fee disputes, the pace of matters or collection delays. The result is a structural mismatch between when value is created and when cash is actually received.

- Work in Progress (“WIP”) - WIP can present additional complexity. Whilst it is an economically real asset, it is not always one that can be valued or realised with certainty. In complex or outcome-dependent matters, the relationship between recorded WIP and eventual cash collection may be highly uncertain. Potential stakeholders therefore tend to approach WIP cautiously, often applying heavy discounts and focusing instead on the firm’s actual billing and collection discipline.

- Lock-up – Lock-up combines WIP lock-up, being the period between work being performed and billed, and debtor or receivables lock-up, being the period between an invoice being issued and It is therefore a measure of how long a firm’s capital is tied up in unbilled work and billed but uncollected receivables. In many law firms, lock-up remains substantial. A business may therefore appear profitable on paper whilst still facing meaningful liquidity strain in practice. That distinction matters: if cash conversion is unpredictable, true debt capacity may be materially lower than headline profitability suggests.

- Asset-light nature - Law firms are, by nature, asset-light. They do not usually own significant property, equipment or inventory that can support secured lending in the traditional sense. Their most important assets are intangible and mobile: client relationships, brand, institutional reputation and the expertise and books of business held by partners and fee earners. From a commercial perspective, these can be excellent assets, however, clients can move, partners can leave and reputation can deteriorate. Whilst security is likely to feature in any law firm investment, for lenders, practical recovery value may therefore be weaker than the legal documentation suggests.

- Billing innovation - Traditional hourly billing, for all its shortcomings, offers a relatively clear link between effort and revenue: time spent can be converted into fees and measured against the underlying cost base. The broader adoption of alternative pricing models adds complexity for valuation and debt capacity. Fixed-fee work, retainers, subscriptions and success-based arrangements may all be commercially attractive, but each changes the financing profile of the business. Fixed fees can compress margins if matters become more complex than expected; retainers and subscriptions may improve liquidity and smooth revenue but can cap upside; and success-based or contingent matters can be highly profitable but create delayed, uncertain and sometimes binary cash flows.

- Regulatory framework – As discussed above, regulatory constraints will often determine how a transaction is structured. Other regulatory aspects will also need to be considered. For example, proactive approval may be required in certain jurisdictions (in the UK, SRA consent will be required where non-lawyers acquire an ownership or voting interest of 10% or more, or an ownership or voting interest entitling that person to exercise “significant influence” over the management of the relevant firm), and restrictions on profit sharing with non-legal practitioners, the treatment of client money, professional obligations and the broader legal-services regulatory framework all introduce additional complexity. These issues will need to be worked through carefully.

- Structure and extraction of profits – Investors will need to analyse how profits can be extracted to cover costs, fund investment, service debt and pay dividends. This is not always straightforward in firms operating through sophisticated frameworks designed to comply with local regulation whilst permitting revenue sharing across multiple jurisdictions. In more complex international structures, “valve partner arrangements” – where a partner acts as a conduit through which partnership profits are allocated and then routed to another person or group (often through a bare trust, nominee, agency or back-to-back contractual arrangement) – and intragroup recharging mechanisms may already exist and will need to be understood. Alternatively, these arrangements may need to be introduced to support the post-deal ownership structure.

- The threat of artificial intelligence - AI presents a material valuation challenge for private equity investment in law firms because it could undermine core assumptions about the traditional legal services business model. Much of law firm value is tied to leverage, utilisation, hourly billing, and the ability to monetise lawyer time on repeatable work such as diligence, document review, research, and drafting. If AI materially reduces the time required for that work, clients may resist paying historic fee levels, compressing revenue and margins even where productivity improves. This creates uncertainty around sustainable earnings, pricing power, staffing models and the durability of partner profits, all of which are central to understanding long-term revenues and valuation. Whilst AI creates opportunities for scale and new service delivery models, it also risks accelerating fee pressure, reducing the economic value of leverage, and shifting legal work toward lower-cost or technology-enabled providers. For investors, an evaluation will need to be made about whether AI enhances a firm’s earnings base or disrupts the very model on which that earnings base has traditionally been valued.

Conclusion

The increasing interest of private capital in legal services reflects a broader shift in how law firms are funded, managed and scaled. The sector’s core attractions are clear: deep client relationships, recurring high-value mandates, resilient demand and scope for operational improvement. For firms facing rising technology, talent, infrastructure and expansion costs, external capital can provide a credible alternative to the traditional reliance on partner capital and retained earnings.

However, legal services are not simply another professional services vertical. Regulation, client relationship dynamics, fee-earner mobility, WIP and lock-up, cash conversion and profit extraction mechanics all create sector-specific complexity for investors and lenders. ABS and MSO structures each provide viable routes into the market, but each carry distinct legal, regulatory, tax and financing implications.

The most compelling opportunities are likely to be those that combine the cultural strengths of a traditional partnership with the discipline of a more institutionalised platform: transparent governance, robust reporting, working capital control, clear profit-sharing mechanics and a credible growth strategy. Private capital is unlikely to replace the traditional law firm model wholesale, but it is broadening the strategic options available to firms and creating new pathways for growth, consolidation, and professionalisation. For investors, it may also offer access to attractive platforms capable of generating meaningful returns, provided the sector’s distinctive legal, regulatory, and commercial risks are properly understood and managed.